Sprinkler Age A Publication of the American Fire Sprinkler Association

Sprinkler Age A Publication of the American Fire Sprinkler Association

Better Business Climate Expectations Help Drive Asset Prices Higher

If someone were casting roles for a production of The Tortoise and the Hare, the U.S. economy would be a favorite to play the tortoise. While this analogy may be a bit harsh, economic growth remains mostly slow, but persistent.

It was not always this way. Based on recently revised data characterizing U.S. GDP, the economy came close to the magical 3 percent threshold – one that it had failed to cross since 2005 – by expanding 2.9 percent in 2015. The year prior, the U.S. economy expanded 2.6 percent. That’s better than turtle speed.

However, last year, the U.S. economy only managed 1.5 percent growth. It then expanded just 1.2 percent during 2017’s initial quarter on an annualized basis, the latest in a string of weak first quarters. In other words, for more than a year, the U.S. economy has been consistently growing at less than 2 percent: Enter tortoise stage right.

That changed, at least temporarily, during the second quarter of 2017. Based on revised estimates from the Bureau of Economic Analysis, the U.S. economy expanded 3 percent on an annualized basis from April through June. As has been the case for several years, much of the progress was driven by growth in consumer outlays. Government spending, by contrast, continues to contribute little, if anything, to the current pace of economic expansion. In fact, based on construction data, investment in a number of publicly financed infrastructure categories has been in decline, including spending on dams and levies, highways and streets, and water systems.

This dynamic has created a dichotomy within the nation’s nonresidential construction industry. While construction firms that focus on private construction activities have seen abundant demand for their services and accompanying lofty backlog on average, firms focused on public construction have been less likely to remain busy. For instance, many heavy highway contractors express disappointment regarding the level of roadwork in the aftermath of the passage of the Fixing America’s Surface Transportation Act in December 2015.

Employment, Wages and Inflation While national output growth has remained erratic, the country continues to add jobs at a healthy clip. Between August 2016 and August 2017, the nation added 2.1 million jobs – impressive given how difficult it has been for construction firms, trucking enterprises, manufacturers, and health care providers to identify available talent.

With the U.S. unemployment rate now below 5 percent (4.7 percent as of September 2017), it’s generally agreed on that the nation is at, or close to, full employment. As available human capital continues to be siphoned off through monthly job growth, the pace of job creation will presumably soften and wage growth will accelerate.

Data indicate that wage pressures are building and that broader inflation expectations are on the rise. Median household income has risen relatively rapidly during each of the past two years. According to the government’s most recent Job Opportunities and Labor Turnover Survey, America boasts 6.2 million job openings – the highest number since the U.S. Labor Department began monitoring job postings in 2000.

Seven million Americans are unemployed, which means that there is almost one job for every person searching for one, implying that the chase for workers will only intensify during the months ahead and that the rate of wage increases is likely to accelerate further. Perhaps in response, the U.S. bond market appears to be pricing in a higher chance of an interest rate hike by the Federal Reserve in December 2017, with the notion being that America’s central bank will perceive a need to continue to take steps to keep problematic inflation at bay.

Some data certainly indicate that inflation expectations and fears are overblown. During the past year, average hourly earnings are up 2.5 percent on a year-over-year basis. That general pace hasn’t moved much during the past few quarters and falls short of the hourly earnings growth that typifies a solidly performing economy. During the months preceding the most recent recession, wage growth consistently exceeded 3 percent. Since 2009, when the economy began its recovery, wage growth has only expanded at a rate of 2.2 percent a year. This is less than wage growth seen in the 1980s (3.3 percent), 1990s, (3.2 percent), and 2000s (3 percent).

The fact that wage growth has failed to accelerate represents one of the nation’s great economic mysteries. There is no shortage of potential explanations, including globalization and overall slower productivity growth. All of these explanations are valid to some extent, but a more likely explanation lies in demographics.

With roughly 10,000 baby boomers turning 65 each day, the number of retirees continues to grow. As younger workers replace older ones, labor costs subsequently fall. Additionally, this helps explain the surprisingly strong corporate profitability, even as the nation’s economy only expands at a rate of 2 percent and while the global economy grows well below 4 percent.

The Construction Case Study Although average wages do not appear to be rising rapidly, the vast majority of construction industry leaders believe the ongoing skills shortage is a major issue.

Here’s a rationale for this apparent inconsistency: As older, more skilled construction workers leave the industry in larger numbers, construction firms are induced to look for replacements.

However, because many younger members of the U.S. labor force have not focused on the acquisition of construction-relevant skills, firms are often hiring on the basis of potential. This process results in enormous training costs and lower industry productivity. It also results in what appears to be smaller wage increases as established, well-compensated talent is replaced by hopefully trainable people entering the industry at lower levels of pay.

When controlling for these compositional effects, wages are rising quite rapidly in the U.S. construction industry. A survey conducted earlier this year by Engineering News-Record suggested that construction firms expected to increase worker compensation in the range of 4 percent to 5 percent in 2017. (See Figure 1.)

Inflation concerns transcend the labor market. Life, in general, appears to be getting more expensive, whether in the form of rising costs for homes, tuition, healthcare, or fuel. Still, through July, the core personal consumption expenditures (PCE) index – the Federal Reserve’s preferred measure of inflation – was up just 1.4 percent, well short of the 2 percent target.

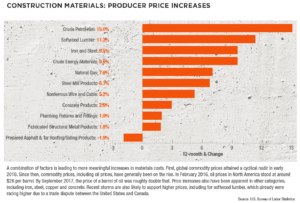

The issue of inflation stands at the heart of the outlook for the U.S. construction industry. America’s recovery is now in its ninth year. U.S. financial indicators, including the Dow Jones Industrial Average and S&P 500 Index, have achieved record highs repeatedly this year. Low interest rates have represented a major factor. With investors suffering difficulty generating investment yield from fixed income assets, many have been chased up the risk spectrum into assets such as commodities, stocks, riskier bonds and commercial real estate. The result has been elevated asset prices, which helps create positive wealth effects for the broader economy and also lifts demand for construction services. However, low interest rates can only persist if inflation remains low. (See Figure 2.)

Construction firms focusing on private segments, such as office and lodging, have frequently flourished as a result. Money has poured into office, hotel, apartment and related segments, driving up asset prices and inducing developers to add rooms and space.

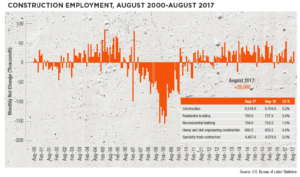

Unfortunately, local, state, and federal governments have failed to takefull advantage of low borrowing costs to invest in infrastructure. Many public construction segments have actually experienced declining construction spending during the past three years, including basic functions like waste disposal and water treatment and delivery. (See Figure 3.)

The ongoing lack of investment in infrastructure positions the U.S. economy to underperform for generations. In its 2017 report, the American Society of Civil Engineers (ASCE) gave U.S. infrastructure a grade of D+. Segments receiving a D+ or below included aviation, dams, drinking water, energy, hazardous waste, inland waterways, levees, public parks, roads, schools, transit, and wastewater. Railroads, which received a B, appear to be the only category in which the United States is keeping pace.

According to the ASCE, the United States will need to spend an additional $1.44 trillion on infrastructure during the next decade to bring its collective public works up to a reasonable standard. If this investment is not met, it could mean the loss of 2.5 million jobs during that period of time.

Looking Ahead For now, the outlook remains stable, and the next year should represent a period of expanding nonresidential construction spending. Associated Builders and Contractors’ Construction Backlog Indicator (CBI) remains elevated. Energy prices have risen, which should position the power sector to be more of a driver of economic activity. Rising home assessments also are boosting local tax collections, which should help stabilize infrastructure spending in many communities.

The broader economy is also in good shape. Increasingly, the worldwide recovery is a synchronized one, with each of the major global economies now expanding. The U.S. economy remains buoyed by confident consumers and rising household incomes. Successful pro-business legislative efforts emerging from Washington, D.C., could serve to further bolster the near-term outlook.

However, the outlook for 2019 and 2020 is hardly guaranteed. Asset prices are high and arguably vulnerable to steep declines. Any number of events could trigger selloffs, including rising inflation/interest rates, North Korea, cyber attacks, or political intrigue. Many construction firm CEOs expect the next year to be good, but believe the current construction spending recovery cycle will be upended at some point within the next three years. n

ABOUT THE AUTHOR: Anirban Basu is chairman & CEO of Sage Policy Group, Inc., an economic and policy consulting firm headquartered in Baltimore, Maryland. The firm provides strategic analytical services to energy suppliers, law firms, medical systems, government agencies, and real estate developers among others. He is also the chief economist to Associated Builders and Contractors (ABC) and chief economic advisor to the Construction Financial Management Association. Visit abc.org/economics.

ABOUT THE AUTHOR: Anirban Basu is chairman & CEO of Sage Policy Group, Inc., an economic and policy consulting firm headquartered in Baltimore, Maryland. The firm provides strategic analytical services to energy suppliers, law firms, medical systems, government agencies, and real estate developers among others. He is also the chief economist to Associated Builders and Contractors (ABC) and chief economic advisor to the Construction Financial Management Association. Visit abc.org/economics.

EDITOR’S NOTE: Reprinted from Construction Executive, December 2017, a publication of Associated Builders and Contractors. Copyright 2017. All rights reserved.